Many investors may have only a qualitative understanding of the ability of indexed fund managers to track the returns of a fixed-income index. Our analysis uses tracking error to provide a quantitative measure of the ease – or difficulty – of consistently tracking an index. We find generally low to moderate tracking error across broad parts of the bond market. Our analysis also suggests that less liquid and higher volatility sectors (such as high yield) tend to have higher tracking error.

We compared returns on taxable U.S. passively managed ETFs across 10 sectors to returns on their underlying benchmarks. For each ETF, we first calculated the annual difference in returns (before fees) relative to its respective benchmark over the past seven years. We then computed the ETF’s tracking error, defined as the standard deviation of its return differences.1 Finally, for each sector, we picked the tracking error for the median ETF. 2 Our sample includes some of the largest ETFs in the market, with a maximum of three ETFs per sector. ETF returns use NAV prices.

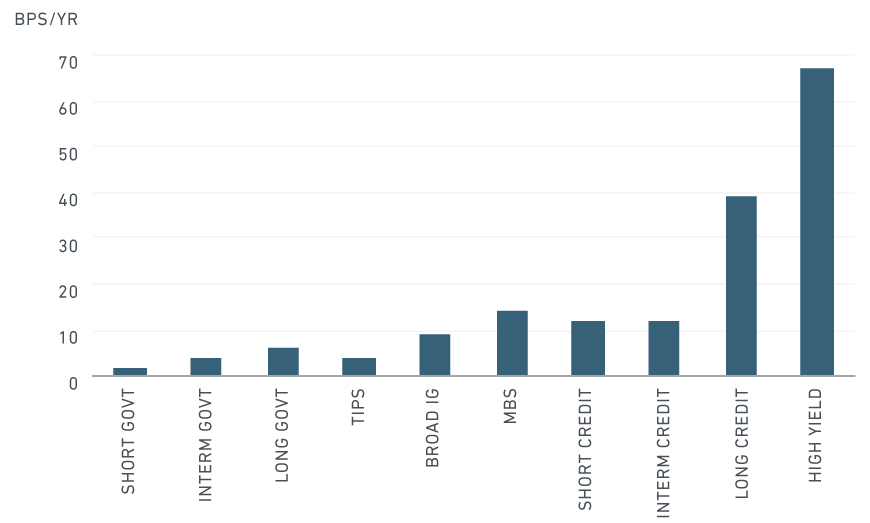

We found that ETFs invested in the government (non-mortgage-backed securities) sectors consistently tracked benchmark performance very closely, with median annual tracking error ranging from 1 to 6 basis points (bps). Tracking error on MBS, broad investment-grade and the short and intermediate credit sectors was modestly higher (ranging from 9 bps to 14 bps) than the government sectors. At 67 bps, the high-yield sector had the highest tracking error, while the long investment-grade credit sector experienced tracking error of 39 bps.

We note that tracking error within a given sector differed among the ETFs in our sample, and so median values may overstate or understate tracking error on other ETFs. For example, ETF tracking error in the high-yield sector ranged from a low of 46 bps to a high of 88 bps.

High yield and long credit were harder to track

Median tracking error over past 7 Years

We use annual data reported to the U.S. Securities and Exchange Commission through Nov. 13, 2017. Different ETFs have different fiscal year reporting periods. The most recent return as of dates ranged from April 30, 2017 to Aug. 31, 2017. In categories with only two ETFs, we show the average tracking error. The returns horizon for TIPS was six years; our sample consisted of 27 ETFs.

What can explain the differences in tracking error between the different sectors? We did not attempt a detailed forensic investigation, but a good starting point for the analysis is to understand that index prices may be based on model estimates. As a result, they may differ from market transaction prices. Particularly in less liquid sectors, managers may find prices on certain bonds in the actual market to be significantly higher or lower than stated index prices.

In the most extreme case, it simply may not be possible to buy a bond; for example, if the bond is held in buy-hold portfolios that allow only limited trading (e.g., in certain insurance company portfolios). Given this possibility or the potential for an expensive transaction price, the fund manager may instead purchase securities with similar but not identical characteristics. The result is that portfolio securities may not be held in strict proportion to their weights in the index. Combined with this mismatch in weights, changes in sector spreads or market events impacting specific issuers or securities may then result in tracking error.

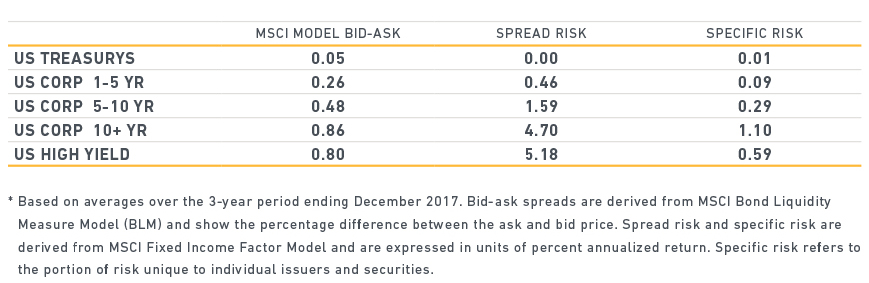

As shown in the figure below, projected spread volatility risk was highest in the high-yield sector; issuer (or security) specific risk was also relatively high. Both of these risk measures systematically increased with the maturity of the credit sector. In addition, liquidity conditions (as proxied by bid-ask spreads) were markedly more favorable in the government bond sector and less favorable in the credit sectors. All in all, these observations on sector volatility risk and liquidity are generally consistent with the patterns in tracking error observed in our sample of ETFs.

Bid-ask, spread risk and specific risk*

Over the next several years, growth in e-trading and regulatory initiatives including MiFID II3 may result in greater price transparency in the fixed-income market. This, in turn, could lead to improved index pricing and stronger portfolio construction tools based on better market liquidity modeling. Particularly for the less liquid parts of the bond market, these developments may help reduce tracking error and may provide investors with a better understanding of sector risk and reward tradeoffs.

The author thanks Aniko Maraz and Juan Sampieri for their contributions to this post.

1 Tracking error is often measured as the annualized volatility of the daily return differences. One reason it may differ from our measure (using annual returns) is if daily return differences are mean reverting. The choice of using one measure over the other should partly depend on the investor’s time horizon.

2 Tracking error penalizes period-by-period fluctuations in return differences. This will be true even if the average portfolio return over the entire time period approximates the index return. The average return difference over the investment horizon is an important measure of performance. Manager skill (e.g., through use of representative sampling techniques) may offset some of the difficulties of managing against an index that is hard to replicate, and may have a greater influence on the long-run average return difference than on tracking error. As a single measure for identifying sectors that are difficult to replicate, we prefer tracking error over the average difference in returns. Discussion of average return differences falls outside the scope of our current post.

3 Effective January 2018, MiFID II introduced a reporting requirement for trade price and size for transactions across the European Union. Proposed rules (still pending SEC approval) from the Public Company Accounting Oversight Board may also contribute to improved fixed-income price transparency. Effective October 2017, the Financial Industry Regulatory Authority (FINRA) reduced the delay period applicable to historic TRACE data for corporate bond transactions from 18 months to six months.

Further reading:

Are corporate bonds vulnerable to ECB tapering?

Managing fixed-income risk in turbulent times

Analyzing credit strategies from a risk and return perspective

The MSCI Bond Liquidity Measure (BLM) (Client access only)